Introduction

Divorce later in life, often called silver divorce or gray divorce, is becoming more common as baby boomers move through retirement. The financial impact can be significant because the same assets that were meant to support one household must now support two.

- Divorce among adults age 50 and older has increased significantly

- Later-life divorce tends to reduce retirement wealth more than earlier divorce

- Poverty rates are materially higher among unmarried retirees

- Women are disproportionately impacted financially after divorce

Research highlighted by financial author Mary Beth Franklin points to several important realities:

For many couples, the home represents the largest asset involved in the settlement. How advisors structure housing decisions can directly affect long-term cash flow, portfolio sustainability, and housing stability.

The following real-world example illustrates three common planning strategies.

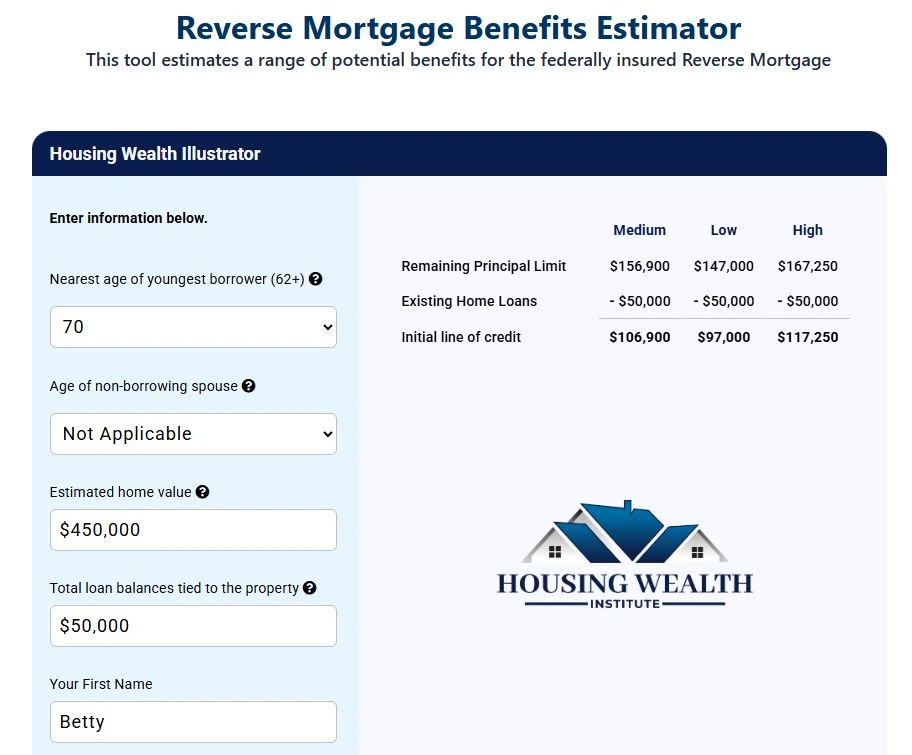

Case Study: Betty and John

Betty (70) and John (71) never expected their 45-year marriage to end, but they now find themselves navigating a gray divorce.

Financial snapshot:

Home value: approximately $450,000

Existing HELOC balance: $50,000

Divorce decree: remaining equity split equally

Goal: Betty would like to stay in the home; John wants to move forward and purchase a new home

How do they divide housing wealth without damaging retirement security?

Three Housing Strategies Advisors Should Consider

Strategy 1: Sell the Home and Divide the Equity

This is the most traditional approach and the one advisors tend to suggest first.

How it works:

Home sold for $450,000

HELOC paid off

Approximately $400,000 remaining equity

Each spouse receives about $200,000

Planning result:

Clean division of assets

Both spouses must secure new housing

May require renting or taking on new mortgage payments

Investment portfolios may be tapped to fund housing

Strategy 2: Spousal Buy-Out Using a Reverse Mortgage

In this strategy, Either spouse remains in the home and uses the reverse mortgage to pay off the other.

How it works:

A reverse mortgage makes a certain amount of dollars available

The existing HECOC is paid off

Remaining proceeds are between $107,000 – $117,000 depending on interest rates at the time

One spouse is owed $200,000

- The reverse mortgage pays the spouse the proceeds and remaining payout is drawn from elsewhere or negotiated.

Planning result:

Housing stability maintained

No new monthly debt obligation

Most portfolio assets remain intact rather than being used for the settlement

This approach can be especially valuable when one spouse wants to stay in the marital home but lacks the cash flow to refinance traditionally.

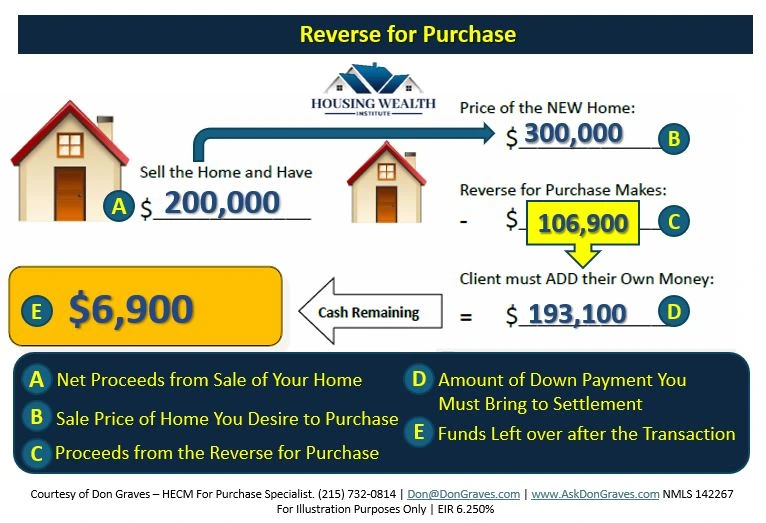

Strategy 3: Either/Both Spouse(s) Use a HECM for Purchase After the Sale

This strategy applies when the marital home is sold and each spouse receives their share of the equity.

How it works:

The home is sold and proceeds are divided according to the settlement

Betty and John each receive their equity share, around $200,000

They each have the option to combine sale proceeds with a HECM for Purchase to buy a new home

The reverse mortgage provides the additional financing needed without creating a mandatory monthly mortgage payment

Planning result:

Both spouses can secure new housing without taking on traditional mortgage debt

Portfolio assets may remain invested instead of being used for full cash purchases

Cash flow flexibility improves during retirement since no required monthly mortgage payment exists

This approach gives both parties the ability to reset their housing situation while preserving liquidity and reducing payment pressure during a financially sensitive transition.

What the Research Says

Researchers and retirement income specialists increasingly recognize housing wealth as an underused planning tool during silver divorce.

Jamie Hopkins, writing in Forbes, cited research from Barry Sacks, PhD, JD, noting that reverse mortgages can provide the liquidity needed to divide housing assets while allowing one spouse to remain in the home without creating monthly payment strain.

Additional work from members of The American College’s Funding Longevity Task Force demonstrates how coordinating reverse mortgage proceeds with IRA or 401(k) withdrawals can improve post-divorce cash flow and reduce retirement stress.

Advisor Takeaways

When working with divorcing retirees:

The home should be analyzed as a financial asset, not just a residence

Reverse mortgages can create liquidity without required monthly payments

HECM for Purchase can help clients secure housing while preserving portfolios

Women, who statistically face greater financial risk after divorce, may benefit from housing-focused strategies

Final Thought

Silver divorce creates financial pressure at a stage of life where recovery time is limited. Advisors who understand housing wealth strategies can offer clients options beyond selling the home or taking on new debt.

The goal is not to make a difficult situation perfect.

It is to create better outcomes from the assets clients already have.

What to Do When You Have a Client or a Case?

- Go to www.HousingWealthPro.com and request a Housing Wealth Illustration. Give Details in the “Notes” Section including the clients’ phone # if they would like a Housing Wealth Assessment. You can also

- Schedule a Time to Speak with Me: Click Here

Related Articles:

Can Reverse Mortgage Proceeds be Used for Financial Products?

Comparing HELOCs and RELOCs for Retirement Income Planning

Case Study: Using Home Equity to Radically Preserve IRA Savings

The content of this blog is for financial advisors and professionals only and is not intended for consumer use. Names, cases, and scenarios are fictionalized for illustrative purposes. The opinions expressed here are those of the author alone and do not reflect the views of any affiliated entities or individuals. Don Graves, NMLS #142667.