Looking Back at 90 Years of Social Security

On August 14, 1935, President Franklin D. Roosevelt signed the Social Security Act into law. Ninety years later, on August 14, 2025, the nation paused to honor its legacy. In his original signing statement, Roosevelt called the act “a cornerstone in a structure which is being built but is by no means complete.” He was right.

For nine decades, Social Security has stood as one of America’s most enduring promises: that after a lifetime of work, citizens should not face old age in poverty. Today it pays benefits to more than 72 million Americans — retirees, disabled workers, and survivors — distributing over $1.6 trillion annually. Yet its future is clouded by financial strain, demographic shifts, and political gridlock. As we celebrate its 90th birthday, the question looms: will Social Security be strong enough for its 180th?

From the Great Depression to Today: A Brief History

Social Security was born in the depths of the Great Depression, when one out of every two elderly Americans lived in poverty. Influenced by grassroots pressure like the Townsend Plan and fueled by Roosevelt’s New Deal, Congress crafted a federal insurance system to provide retirement benefits funded by payroll contributions.

Key milestones along the way include:

- 1939 Amendments: Extended benefits to spouses, widows, and dependents, making it a family-based program rather than an individual one.

- 1965 Amendments: Introduced Medicare and Medicaid, expanding the safety net for health care.

- 1972 Reform: Added automatic cost-of-living adjustments (COLAs) tied to inflation, ensuring benefits kept pace with rising prices.

- 1983 Amendments: A bipartisan rescue under President Reagan and Speaker Tip O’Neill. These changes gradually raised the full retirement age, increased payroll taxes, and extended coverage to more federal workers. They temporarily restored solvency but foreshadowed today’s challenges.

- 2025 Social Security Fairness Act: Repealed the Windfall Elimination Provision (WEP) and Government Pension Offset (GPO), restoring benefits for millions of public-sector retirees. While celebrated for fairness, it also added strain to the trust fund.

From its modest beginnings, Social Security has evolved into the backbone of American retirement — for many, the single largest source of income in old age.

A Human Lens: Ida May Fuller and Today’s Choices

Every program needs a face, and for Social Security that face is Ida May Fuller.

In January 1940, Ida, a retired legal secretary from Vermont, picked up the very first Social Security check: $22.54. She had contributed only $24.75 in payroll taxes but lived to age 100, collecting nearly $23,000 in benefits. Her story captures the insurance nature of Social Security: a community pooling of resources to ensure dignity in old age.

Fast-forward to today, and the questions facing recipients are less about eligibility and more about when to claim.

- Claiming at 62: The earliest possible age, but with a 25–30% permanent reduction.

- Claiming at 67 (Full Retirement Age): No reduction, but no bonus either.

- Claiming at 70: With delayed retirement credits of about 8% per year, benefits can be 24–32% higher than at full retirement age.

Another factor too often ignored: the spouse. When one spouse dies, the survivor inherits the higher benefit. That makes the higher earner’s claiming decision critical for the household’s long-term security.

Current Challenges: The Solvency Squeeze

Despite its success, Social Security faces a stark financial reality. The Old-Age and Survivors Insurance (OASI) Trust Fund is projected to be depleted by 2033 (or 2034 under alternate assumptions). Without reform, benefits will be automatically cut by about 20–23%.

Why? Three forces collide:

- Demographics: Baby Boomers are retiring, birth rates are lower, and people live longer. In 1950, there were 16 workers per retiree; today there are fewer than three.

- Economics: Payroll taxes fund the system, but wage growth hasn’t kept pace with benefit promises.

- Policy choices: Expansions like the 2025 repeal of WEP/GPO and tax relief for seniors, though popular, reduce revenue and accelerate depletion.

Potential Paths Forward: Securing the Next 90 Years

Reform is not optional. The only question is which combination of changes lawmakers will choose. Options include:

- Raise payroll taxes.

- Gradually increase the retirement age.

- Modify COLAs or high-earner benefits.

- Lift or remove the wage cap on taxable income.

- Introduce investment options or personal accounts.

- Blend revenue and benefit changes, much like the 1983 compromise.

Conclusion: A Promise Worth Keeping

At 90, Social Security remains one of the most popular and effective government programs in American history. It has cut elder poverty dramatically, supported widows and orphans, and given generations of workers confidence that their contributions matter.

But anniversaries are not just for celebration — they are also for reflection. Without timely reform, today’s workers could face deep benefit cuts in just a decade. With courage and foresight, we can secure the program for another 90 years.

Reprinted with permission.

Author: David P. Zander, CFP® Emeritus Board™

Email: dzander@back9pro.com

Phone: 260-615-0078

Original post date: September 22, 2025

Source: Back9Pro

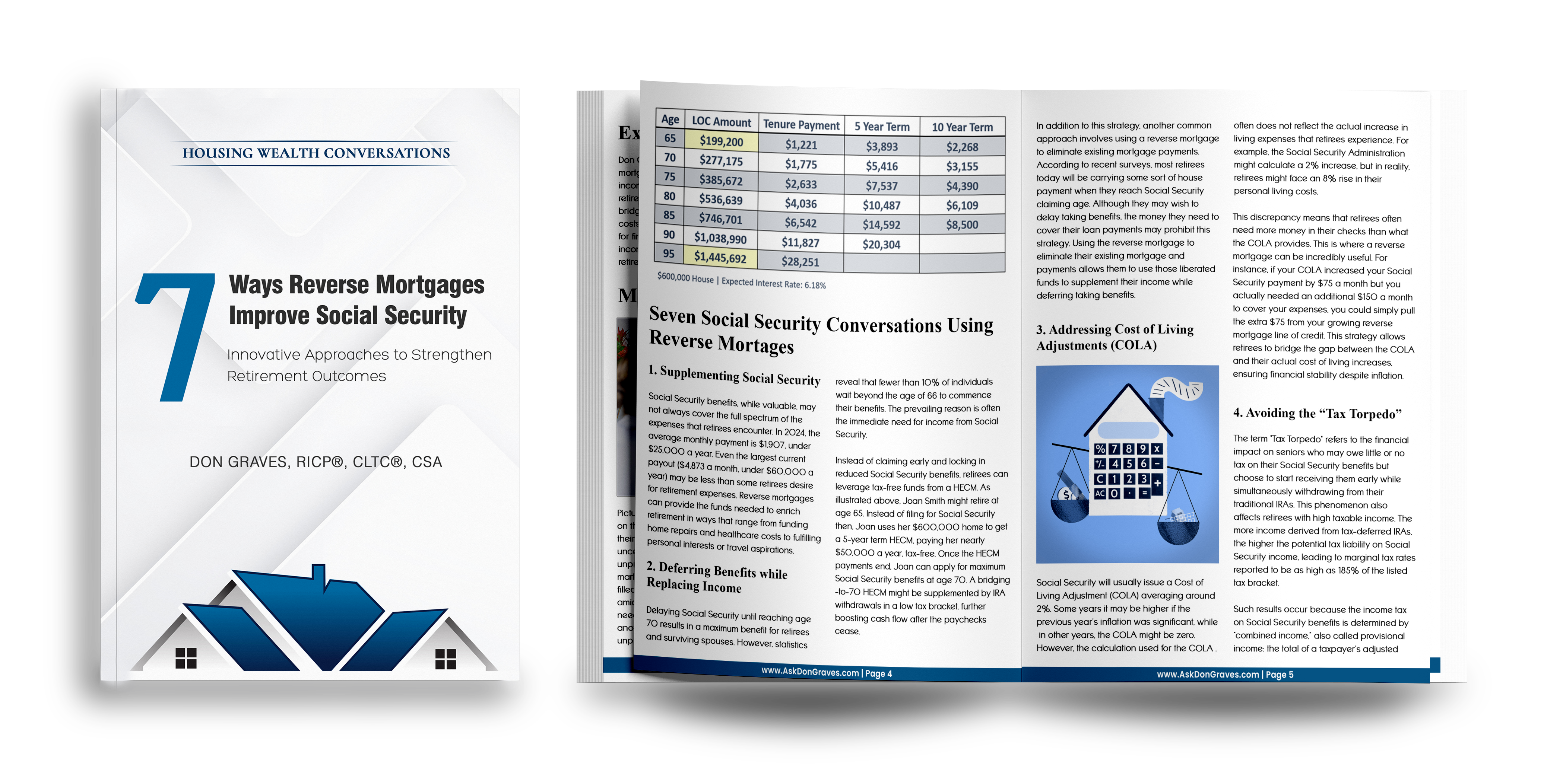

Free Report for Download: 7 Ways Reverse Mortgages Improve Social Security Planning

Learn how reverse mortgages can enhance your Social Security strategy with our free report, “7 Ways Reverse Mortgages Improve Social Security Planning.” Discover practical strategies to:

(If you are unable to download the article, Please Click Here and we will get it to you another way)

Related Articles and Resources

What to Do When You Have a Client or Case?

- Go to www.HousingWealthPro.com and request an Housing Wealth Illustration. Give Details in the “Notes” Section including the clients phone # if they would like a Housing Wealth Assessment. You can also

- Schedule a Time to Speak with Me: Click Here

The content of this blog is for financial advisors and professionals only and is not intended for consumer use. Names, cases, and scenarios are fictionalized for illustrative purposes. The opinions expressed here are those of the author alone and do not reflect the views of any affiliated entities or individuals. Don Graves, NMLS #142667.