What Can a Tax Return Reveal About Retirement Readiness?

Advisors do not need to be CPAs to recognize when something is off in a retiree’s financial picture. Quite often, the first warning signs appear not in a portfolio statement or a Social Security projection, but in the tax return. For clients over 62, the 1040 is more than a document to be filed and forgotten. It is a map of financial stress points that most advisors walk right past.

Tax returns can reveal unsustainable drawdown rates, bracket creep from RMDs, heavily taxed Social Security benefits, mandatory mortgage payments draining monthly cash flow, a quiet and growing anxiety about outliving savings. These are not abstract planning concerns. They appear in black and white on a document clients hand their accountant every spring, and they often point toward one largely overlooked source of relief: housing wealth.

What Is a Reverse Mortgage?

A reverse mortgage is a federally insured loan for homeowners age 62 or older that allows them to convert a portion of their home’s equity into tax-free cash—without selling the home, giving up ownership, or taking on a required monthly mortgage payment.

The amount available is based on three key factors: the age of the youngest borrower (or eligible non-borrowing spouse), the value of the home, and current interest rates. For example, a 70-year-old couple with a $850,000 home might qualify for approximately $345,000 to $308,000 in reverse mortgage proceeds at today’s rates.

Because a reverse mortgage must be the first mortgage on the property, any existing loans will be paid off at closing. Whatever is left becomes accessible as a growing, tax-free line of credit that can be used at any time—for income, emergencies, Roth conversion taxes, long-term care costs, or simply as a standby reserve.

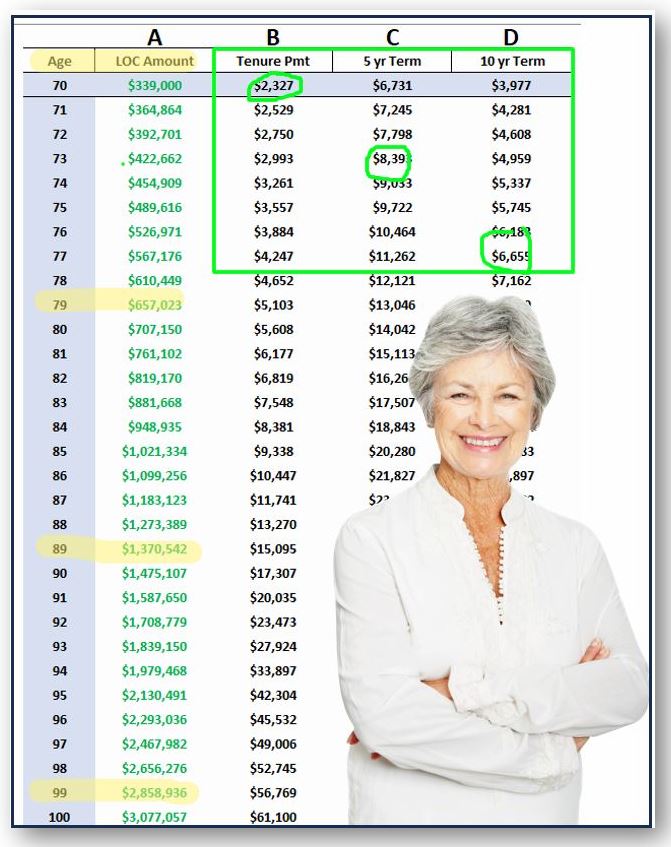

The Growing Line of Credit (GLOC)

Below is an example of a initial line of credit of $339,000 and its potential growth (A) and convertibility (B,C,D) which shows how in any given year the GLOC could be converted into a monthly payment for the Life of the Loan (B) or 5 and 10 years draw periods (C/D) The truth is that this is just a snapshot of the flexibility of the reverse mortgage line of credit as a retirement planning resource.

Why This Matters for Tax Pros

Most homeowners over 62 are sitting on hundreds of thousands—sometimes millions—in home equity. And yet, many of these same clients are:

- Drawing down taxable accounts too quickly

- Paying more in taxes than necessary

- Postponing needed care

- Quietly worried they’ll outlive their savings

As a reverse mortgage educator and planner with 25 years of experience, I can tell you: when used strategically, a reverse mortgage becomes more than a last resort—it becomes a tax-optimized, cashflow-flexible retirement planning tool.

So how do you know when to bring it up?

The following list is not exhaustive, and it is not a sales checklist. It is a set of conversation prompts. Each item represents a pattern that may appear in a client’s return and that could indicate a meaningful role for a housing wealth strategy. Some items will overlap. Many will not apply to every client. But when several appear together, the return is telling you something worth exploring.

15 Clues Hidden in the 1040 That May Call for a Reverse Mortgage Conversation

Does your client…

- Own a home with significant equity? Home equity is often the largest asset on the balance sheet and the last one anyone examines in a planning conversation. If the return shows a client drawing down investments while sitting on hundreds of thousands in untapped home equity, the math deserves a second look.

- Carry a monthly mortgage payment that strains cash flow? A mandatory mortgage payment creates a fixed drag on monthly income that compounds over time. If the return shows a client juggling that payment alongside limited retirement income, the question of whether that obligation needs to remain mandatory is worth asking.

- Show taxed Social Security benefits due to excess provisional income? When up to 85 percent of a Social Security benefit is being taxed, it is often because other income sources are pushing the client over provisional income thresholds. Reducing taxable withdrawals through a housing wealth strategy can help bring that exposure back down.

- Appear to be on the edge of a higher tax bracket? RMDs, investment income, and part-time work can all conspire to push a client into a higher bracket in retirement. A tax-free source of liquidity can serve as a pressure valve, helping manage bracket exposure without reducing lifestyle.

- Show regular withdrawals from retirement accounts to meet everyday needs? Consistent IRA or 401(k) draws for routine expenses suggests the client’s income floor may not be keeping pace with spending. It also suggests that a tax-free supplement could meaningfully reduce the long-term tax cost of retirement.

- Lack sufficient assets to confidently sustain income through full life expectancy, plus five years? Longevity risk does not always announce itself. But a careful look at the return, combined with a projection of assets versus spending, can reveal a gap the client has not yet fully confronted. Housing wealth can help extend the runway without requiring a major change in behavior.

- Have a spouse whose death would reduce household income but not expenses? Survivor income risk is one of the most underappreciated planning gaps in retirement. A surviving spouse often loses one Social Security benefit while fixed expenses remain largely unchanged. A housing wealth reserve can provide critical support when that transition occurs.

- Lack liquid, non-taxable resources for medical or emergency needs? Most retirees have assets, but not all of those assets are accessible without a tax cost. A tax-free line of credit secured by home equity can serve as a standing emergency reserve that generates no income when it is not being used.

- Show no plan for long-term care expenses? Long-term care is among the most expensive and least planned-for risks in retirement. If the return shows a client with limited liquid assets and no coverage in place, the home may represent one of the few remaining options for funding future care needs.

- Mention downsizing or relocating for financial reasons? When a client is considering selling the family home simply to free up cash, it is worth asking whether a housing wealth strategy could accomplish the same financial goal without requiring a move the client does not actually want to make.

- Want to pursue Roth conversions but hesitate because of the tax cost? Roth conversions are among the most powerful tax planning tools available in retirement, but the upfront tax cost creates real hesitation. Tax-free proceeds from a housing wealth strategy can fund conversion taxes without pulling money from the portfolio.

- Have a portfolio too concentrated in market-exposed assets with no buffer? Sequence of returns risk is most dangerous early in retirement, when large withdrawals from a declining portfolio permanently impair its recovery. A housing wealth reserve can serve as a buffer, allowing the client to avoid selling investments at the wrong time.

- Show drawdown patterns that risk penalties or long-term tax inefficiency? Certain withdrawal patterns can trigger IRMAA surcharges, capital gains exposure, or other unintended consequences. Reviewing those patterns alongside a housing wealth conversation can open options that pure portfolio management cannot address on its own.

- Express a desire for one more tax-free bucket of money? Clients often articulate this need without knowing what to call it. They want flexibility. They want a reserve that does not create taxes when they access it. A reverse mortgage line of credit can be exactly that resource.

- Carry financial stress they have not yet named? Not every clue in a return is a specific line item. Sometimes it is a pattern, a combination of factors that together suggest a client who is managing carefully but without much margin. That is often the client most likely to benefit from a conversation about housing wealth, and the one least likely to bring it up on their own.

Five Case Studies That Bring These Ideas to Life

Case Study 1: Bill and Sandy, 65/63 | Newly Retired

Bill and Sandy scheduled a review meeting after visiting their accountant. When their advisor reviewed the return, he asked if their retirement dreams had changed.

They admitted they felt a little concerned about unexpected expenses, long-term care, and whether they’d outlive their savings.

Their advisor noticed they were still paying a $1,500 mandatory monthly mortgage payment. When asked if they’d prefer that payment to be mandatory or voluntary, they quickly answered, “Voluntary!”

He showed them a Customized Housing Wealth Illustration that addressed all three concerns without changing their financial behavior. They were amazed how one overlooked asset could create such peace of mind.

Case Study 2: Evelyn, 72 | Widow, Retired Librarian

Evelyn’s tax return showed her Social Security was being heavily taxed due to IRA withdrawals. With no long-term care coverage and few liquid assets, she was concerned about future expenses but hesitant to touch her remaining savings.

Her advisor introduced a housing wealth strategy using her paid-off $650,000 home. It created a tax-free reserve and allowed her to reduce taxable withdrawals without sacrificing her lifestyle.

Tears welled up as she said, “I never imagined my home could take care of me the way I took care of it.”

Case Study 3: Greg and Darlene, 68/66 | Small Business Owners

Greg and Darlene’s tax return showed rising income and a looming RMD problem. They wanted to do Roth conversions but didn’t want the tax hit.

Their advisor asked, “What if you didn’t have to touch your portfolio to cover the taxes?”

By accessing equity in their $850,000 home, they funded a 5-year Roth strategy, reduced lifetime taxes, and protected their legacy—without drawing down investments.

Case Study 4: Bob and Sally, 73 | Retired Couple

Bob and Sally live in a $700,000 home with a $200,000 mortgage. Their tax return showed interest deductions but also flagged excess IRA withdrawals that increased their tax bill.

They were “just trying to be safe,” they said. Their advisor showed how eliminating the mortgage payment through a reverse strategy could reduce taxable income and provide flexibility for future needs.

They responded, “Why didn’t anyone tell us this sooner?”

Case Study 5: Bill, 68 | Retired Engineer

After selling highly appreciated stock to cover a family expense, Bill was shocked by the capital gains taxes. His advisor asked, “What if there was a way to access funds for future needs—without creating more taxes?”

A housing wealth strategy allowed Bill to create a liquid, tax-free buffer and preserve his portfolio for future growth.

The Tax Return Is More Than Math—It’s a Map

Every 1040 tells a story, not only about what has been earned or spent, but about where a client is headed and whether their current plan is likely to get them there. The fifteen items above are not diagnostic criteria. They are invitations to look more carefully and to ask questions that most advisors are not yet asking.

A reverse mortgage is not the right answer for every client who appears on this list. But for the right client, at the right moment, it can create meaningful flexibility, reduce unnecessary tax exposure, and turn a dormant asset into an active planning resource.

The conversations in this book are designed to help you recognize those moments. The 1040 is a good place to start looking for them.

What to Do When You Have a Client or a Case?

- Go to www.HousingWealthPro.com and request a Housing Wealth Illustration. Give Details in the “Notes” Section including the clients’ phone # if they would like a Housing Wealth Assessment. You can also

- Schedule a Time to Speak with Me: Click Here

Related Articles:

- Seven Ways to Lower Retirement Taxes With a Reverse Mortgage

- Creating a Long-Term Care Health Plan with Reverse Mortgages

- How to Uncover the Social Security Time Bomb

The content of this blog is for financial advisors and professionals only and is not intended for consumer use. Names, cases, and scenarios are fictionalized for illustrative purposes. The opinions expressed here are those of the author alone and do not reflect the views of any affiliated entities or individuals. Don Graves, NMLS #142667.