Surprise

One of the most common surprises for homeowners and advisors today is discovering that a reverse mortgage does not produce enough proceeds to fully pay off an existing loan.

With higher interest rates, this situation is becoming more common. Clients often assume that strong home equity automatically means the reverse mortgage will eliminate their payment. Sometimes it does. Sometimes it doesn’t.

When it doesn’t, the industry calls it being “short to close.”

The good news is this is not the end of the conversation. It simply means there are planning decisions to make.

Why the Reverse Mortgage Didn’t Pay Off the Loan

Understanding How Benefits Are Calculated

Reverse mortgage proceeds are not based on what a homeowner owes. They are determined primarily by three factors:

- The age of the youngest borrower

- The value of the home (up to lending limits)

- Current interest rates

The older the borrower, the more may be available. Higher interest rates generally reduce available proceeds. The existing mortgage balance is not part of the calculation. It simply must be paid off at closing.

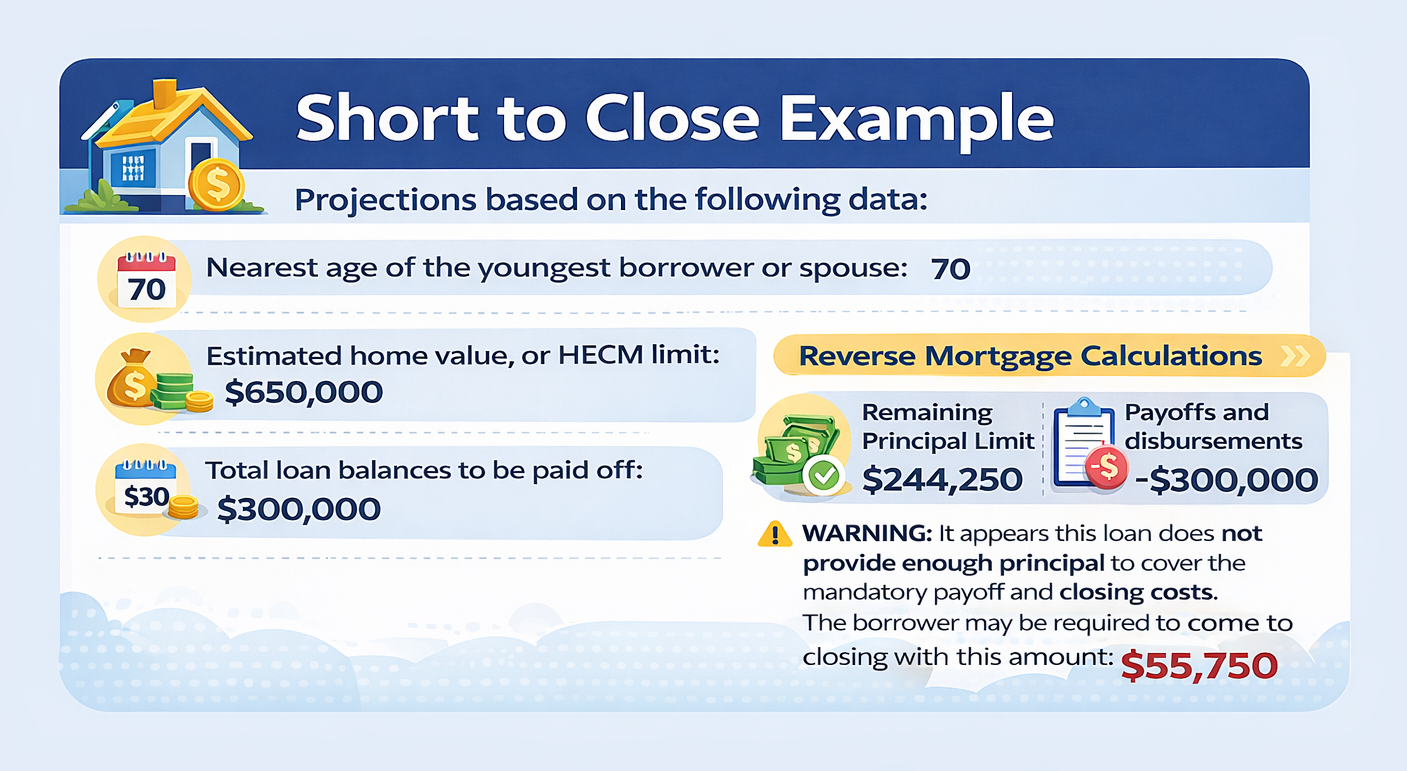

Consider this example.

A couple, both age 70, owned a $650,000 home. They carried a $300,000 mortgage and were making $2,500 monthly principal and interest payments. Their goal was straightforward: eliminate the payment and improve retirement cash flow so they would not have to continue pulling after-tax dollars from retirement savings.

They entered their numbers into the reverse mortgage calculator at www.HousingWealthCalculator.com.

The results surprised them.

Based on their age, home value, and current rates, the reverse mortgage did not generate enough proceeds to pay off the existing loan. They were short by approximately $55,750.

This is not uncommon.

Many homeowners assume reverse mortgages work like traditional refinances where equity alone determines borrowing power. In reality, the calculation is actuarial, built around age and interest rate assumptions.

Once they understood that, the conversation shifted from disappointment to planning.

Because when you are short to close, you still have options.

Option 1: Wait

Sometimes the best choice is patience.

Home values may rise. The existing mortgage balance may decline. Age-based proceeds may improve over time.

If the current payment is manageable, waiting two or three years can materially change the numbers.

Waiting is not always ideal, but it is a valid strategy.

Option 2: Hope for a Higher Appraisal

Some homeowners hope the appraisal will come in higher than expected and close the gap.

While that can happen occasionally, it is not a reliable strategy. Experienced professionals usually have a reasonable sense of value before the appraisal ever arrives.

Hope is not a plan.

Option 3: Sell and Move (HECM for Purchase)

For some families, the better solution is not to force the numbers to work in the current home.

Instead, they sell, capture their equity, and purchase a new home using a HECM for Purchase strategy.

This allows them to:

- Use sale proceeds as a down payment

- Purchase a new home with no mandatory monthly mortgage payment

- Improve cash flow immediately

Many retirees find this approach simplifies their financial picture and aligns better with the next stage of retirement.

Option 4: BYOB — Be Your Own Bank

This is often the most overlooked option.

If homeowners have available liquid assets, they can bring funds to closing to eliminate the shortfall themselves.

In this case, the couple could choose to bring approximately $55,000 to close.

The natural question is:

Why would someone use their own money?

Here are four practical reasons.

- They have the resources.

If funds are available without creating hardship, this option becomes possible. - They are already making a payment.

They were already paying $2,500 every month. That payment was already impacting retirement cash flow. - They control the terms.

By becoming their own bank, they decide if and when to replenish their savings. There is no required repayment schedule. - It can be temporary.

Think of it as borrowing from yourself. If they choose to “pay themselves back” using what used to be the mortgage payment, the funds can be restored over time while still enjoying the flexibility created by the reverse mortgage.

The Bigger Planning Conversation

When a reverse mortgage doesn’t fully pay off an existing loan, many people assume the strategy has failed.

In reality, this moment often opens the door to better planning.

The goal is not simply to close a loan. The goal is to create flexibility:

- Reduce pressure on retirement withdrawals

- Improve monthly cash flow

- Protect portfolios from unnecessary strain

- Give retirees more control over financial decisions

Each option carries trade-offs. Waiting may improve numbers later. Moving may create a cleaner solution. Bringing funds to close may create immediate flexibility.

The right answer depends on the client’s goals, liquidity, and overall retirement plan.

Final Thought

Being short to close is not a problem. It is a planning crossroads.

Once homeowners and advisors understand how reverse mortgage benefits are calculated, the conversation changes. Instead of asking, “Why didn’t this work?” the question becomes, “Which option works best for our plan?”

And that is where good retirement planning begins.

What to Do When You Have a Client or a Case?

- Go to www.HousingWealthPro.com and request a Housing Wealth Illustration. Give Details in the “Notes” Section including the clients’ phone # if they would like a Housing Wealth Assessment. You can also

- Schedule a Time to Speak with Me: Click Here

Related Articles:

Can Reverse Mortgage Proceeds be Used for Financial Products?

Comparing HELOCs and RELOCs for Retirement Income Planning

Case Study: Using Home Equity to Radically Preserve IRA Savings

The content of this blog is for financial advisors and professionals only and is not intended for consumer use. Names, cases, and scenarios are fictionalized for illustrative purposes. The opinions expressed here are those of the author alone and do not reflect the views of any affiliated entities or individuals. Don Graves, NMLS #142667.

2 thoughts on “When Reverse Mortgage Proceeds Don’t Pay Off the Existing Mortgage: Four Planning Options”

Male 82

single

NT

Home $1.1 Million

Mortgage $500K

will HECM work

Thanks

Hi Arun, we will reach out!