Video: The New Reverse Mortgage Borrower

Reverse Mortgages Have Evolved: A New Era of Retirement Planning

When reverse mortgages were introduced in 1961, they were a niche solution primarily designed to help widows stay in their homes. Over the decades, the program has undergone significant structural and regulatory changes, making it a far more versatile financial tool than it once was.

When I first began working with reverse mortgages in 2000, the industry was still clouded by misconceptions. Many saw them as a last resort for cash-strapped retirees. But today’s reverse mortgage is a completely different tool—one backed by decades of research, enhanced government oversight, and increasing adoption by financial professionals.

This evolution has broadened who reverse mortgages serve and how they are used. No longer just a solution for those in financial distress, reverse mortgages now provide flexibility, security, and efficiency for a wide range of retirees. Whether it’s eliminating a mortgage payment, optimizing tax strategies, or securing long-term care funding, home equity is a powerful yet often overlooked asset in retirement planning.

Helping Clients See Reverse Mortgages Differently

As a financial advisor, you’ve likely encountered clients who are hesitant or skeptical about reverse mortgages. They may ask, “Aren’t those just for people who are out of options?”

This outdated perception still lingers, but the reality is that reverse mortgages have become a strategic financial tool used by a diverse range of retirees. Instead of being a last resort, they are increasingly recognized as a proactive way to enhance financial security, increase liquidity, and protect investment portfolios from sequence risk.

The Four Key Ways Reverse Mortgages Serve Retirees

Before exploring the five key borrower profiles, it’s important to frame reverse mortgages in a way that resonates with your clients. These tools aren’t just about solving problems—they’re about creating opportunities and enhancing financial well-being.

Here are four key ways a reverse mortgage can serve retirees:

✅ Solve a Problem: For clients with immediate financial needs, a reverse mortgage can eliminate a monthly mortgage payment, cover medical expenses, or fund necessary home repairs—providing financial relief without liquidating investments.

✅ Bridge a Gap: Many retirees face temporary liquidity challenges, such as waiting for a home sale, delaying Social Security for higher benefits, or navigating a market downturn. A reverse mortgage provides short-term financial flexibility.

✅ Insure Against Risk: Housing wealth can serve as a safety net for unexpected expenses, such as healthcare costs, long-term care, or market volatility. A reverse mortgage line of credit ensures retirees won’t have to drain other assets in times of need.

✅ Fulfill a Desire: Retirement is about more than just covering expenses. Reverse mortgages can help retirees fund lifestyle goals, such as travel, charitable giving, or leaving a meaningful legacy for their family—without depleting their investment portfolio.

As an advisor, your role is to help clients see beyond the misconceptions and recognize how reverse mortgages can integrate seamlessly into their overall financial strategy.

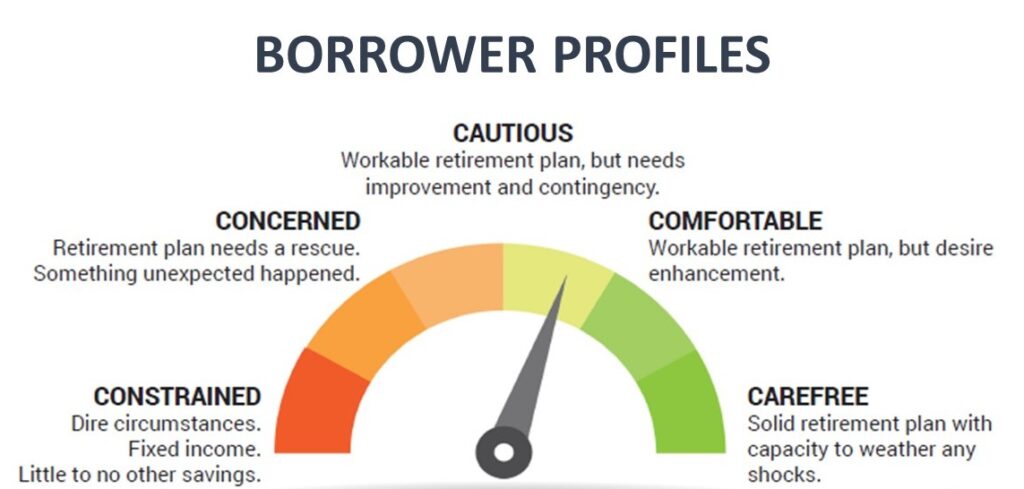

5 Profiles of the Modern Borrower

1. The Constrained Borrower

Who They Are: Meet Mary, a 72-year-old on a fixed income. Her Social Security barely covers her living expenses, and unexpected home repairs have left her financially overwhelmed. A reverse mortgage allowed her to pay off lingering credit card debt and fund critical repairs.

Advisor’s Opportunity: For clients like Mary, reverse mortgages can provide immediate relief and restore financial stability. You can frame it as a tool to eliminate debt and cover necessary expenses.

How They Use Reverse Mortgages:

- Cover basic living expenses.

- Pay off existing debt to reduce financial stress.

- Handle emergencies like medical bills or home repairs.

Mary’s Words: “This was a lifeline for me. I’m no longer constantly worried about making ends meet.”

2. The Concerned Borrower

Who They Are: Bob and Susan are financially stable today but worry about potential healthcare costs or other unforeseen events. They decided to set up a reverse mortgage line of credit as a “safety net” for peace of mind.

Advisor’s Opportunity: For clients who value financial security, you can present reverse mortgages as a proactive way to prepare for the unexpected. Highlight the value of having a growing line of credit.

How They Use Reverse Mortgages:

- Establish a line of credit for future needs.

- Create a financial buffer against market volatility.

- Reduce financial stress about “what if” scenarios.

Bob’s Words: “We may never need it, but knowing it’s there helps us sleep at night.”

3. The Cautious Borrower

Who They Are: Emily, a retired teacher, has a solid retirement plan but is looking for ways to optimize it. Her advisor recommended a reverse mortgage to reduce taxable withdrawals and maximize her portfolio’s longevity.

Advisor’s Opportunity: For cautious planners, reverse mortgages can complement their existing strategies. Emphasize how they reduce pressure on retirement assets and optimize tax efficiency.

How They Use Reverse Mortgages:

- Reduce portfolio withdrawals to preserve growth.

- Fund Roth IRA conversions to lower future tax burdens.

- Delay claiming Social Security for higher payouts.

Emily’s Words: “It’s not about survival; it’s about being smart with my money.”

4. The Comfortable Borrower

Who They Are: Paul and Diane are financially secure and living comfortably in retirement. Their reverse mortgage funded a six-week European vacation while preserving their investments for their children.

Advisor’s Opportunity: For these clients, reverse mortgages enhance retirement enjoyment without depleting assets. Present it as a way to strike a balance between lifestyle and legacy goals.

How They Use Reverse Mortgages:

- Fund travel or bucket-list experiences.

- Create a financial cushion for market downturns.

- Preserve assets for inheritance planning.

Diane’s Words: “It let us enjoy life now without worrying about impacting what we leave behind.”

5. The Carefree Borrower

Who They Are: Jack, a retired executive, has significant wealth but sees his home equity as an untapped resource. He uses a reverse mortgage to fund investment opportunities and optimize his tax strategy.

Advisor’s Opportunity: For affluent clients, reverse mortgages are strategic tools. Highlight how they can enhance wealth management and estate planning.

How They Use Reverse Mortgages:

- Access low-cost funds for investments.

- Optimize tax and estate planning strategies.

- Pass on assets more efficiently to heirs.

Jack’s Words: “It’s about financial efficiency. Why wouldn’t I use all the tools available?”

Reframing the Reverse Mortgage Conversation

Is there an ideal borrower for a reverse mortgage? No! As a financial advisor, you have the power to help clients see reverse mortgages in a new light. Whether your client is constrained, cautious, or carefree, housing wealth can play a pivotal role in their financial plan. Reverse mortgages are:

- Flexible: Adaptable to a variety of client goals.

- Strategic: Complementary to retirement and wealth-building strategies.

- Empowering: Helping clients live the retirement they envision.

Every client’s story is unique. By introducing reverse mortgages as part of a holistic financial plan, you can provide innovative solutions that align with their goals. Ready to start the conversation? Let’s explore how this tool fits into your clients’ needs.

What to Do When You Have a Client or a Case?

- Go to www.HousingWealthPro.com and request a Housing Wealth Illustration. Give Details in the “Notes” Section including the clients’ phone # if they would like a Housing Wealth Assessment. You can also

- Schedule a Time to Speak with Me: Click Here

Related Articles:

- How Did Reverse Mortgages Get Such a Bad Reputation?

- 37 Frequently Asked Questions About Reverse Mortgages

- Why Waiting to Secure a Reverse Mortgage Could be a Costly Mistake

The content of this blog is for financial advisors and professionals only and is not intended for consumer use. Names, cases, and scenarios are fictionalized for illustrative purposes. The opinions expressed here are those of the author alone and do not reflect the views of any affiliated entities or individuals. Don Graves, NMLS #142667.